Fed says September cut 'on the table'

Plus: Middle East tensions surge as Iran vows harsh retaliation for Hamas hit; Doubts over competing Paramount bid; Boeing taps retired industry veteran Kelly Ortberg for turnaround.

Good morning. Here's what happened overnight and what you need to know today.

1.

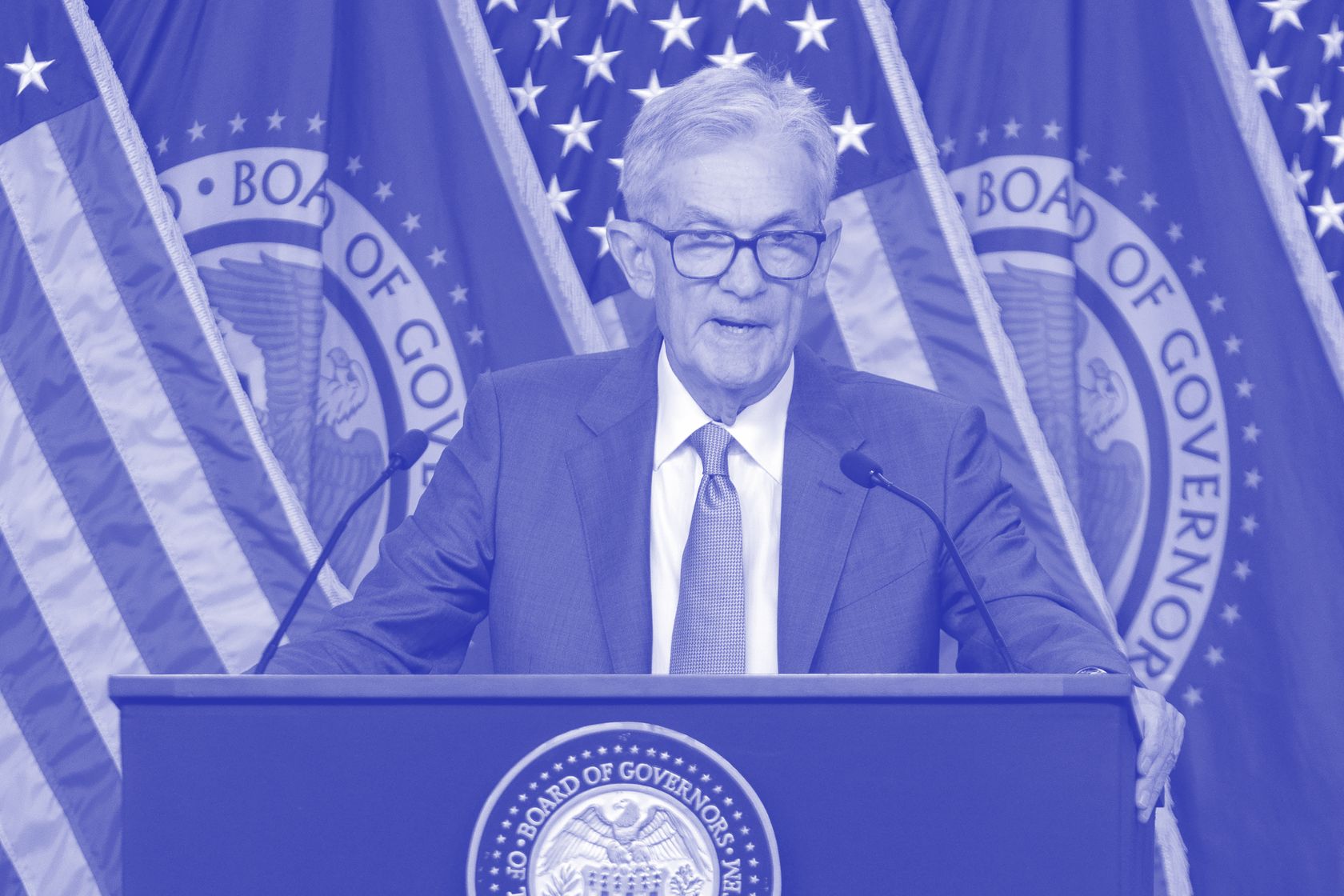

Fed holds: The Federal Reserve held US interest rates steady at 5.25% to 5.5%, the highest in over 20 years and the rate it has maintained for the past year, but signalled the potential for a cut in September amid easing inflation and a cooling job market. The Federal Open Market Committee’s (FOMC) decision was unanimous, according to its statement, which underscored risks to both inflation and employment, suggesting a more balanced approach to its dual mandate. The bank acknowledged progress toward its 2% inflation target in the past year but noted inflation remains “somewhat elevated”. The labour market has shown welcome signs of cooling, it said, with job gains moderating and the unemployment rate rising to 4.1%. Despite that, the Fed’s statement repeated it would not lower rates until there is “greater confidence” that inflation is moving sustainably towards its 2% target. “We are not there yet,” Fed Chair Jerome Powell said at a press conference after the announcement. He then added “we think that the time is approaching.. (and a cut) could be on the table at the September meeting.” Two-year Treasury yields moved lower and the S&P 500 index rose after his comments, according to Bloomberg data. The dollar remained lower. (Capital Brief)(Bloomberg)

2.

Middle East tensions: Iran’s Supreme Leader Ayatollah Ali Khamenei vowed "harsh punishment" following the assassination of Hamas leader Ismail Haniyeh in Tehran, Iranian state media reported. Khamenei said Iran was duty-bound to avenge Haniyeh, whose killing, while he was attending the inauguration of Iran’s newly elected president, he attributed to Israel. The assassination came shortly after an Israeli airstrike killed a senior Hezbollah official in Beirut. The dual strikes have heightened regional tensions, putting the Middle East on the brink of wider conflict. The US, which has been actively mediating to prevent escalation, was not informed of Haniyeh's killing in advance, Secretary of State Antony Blinken said. He urged Qatar, a mediator in Gaza cease-fire talks, to persist despite the escalation. Qatar’s prime minister, Mohammed bin Abdulrahman bin Jassim Al Thani, asked on social media: “Can mediation succeed when one party assassinates the negotiator on the other side? Peace needs serious partners & a global stance against the disregard for human life.” (Capital Brief)

3.

Paramount drama: Shares in Paramount Global rose as much as 4% to USD11.7 ($17.91) on Wednesday after Reuters reported an investor – Apex Capital Trust – had submitted an offer to acquire Paramount Global for up to USD43 billion. The reported new bid follows extended negotiations between David Ellison’s Skydance Media and Shari Redstone’s National Amusements to acquire Paramount that last month resulted in a merger agreement, that included a 45-day "go-shop" period for alternative offers. According to the report Apex's all-cash offer includes buying National Amusements, which controls Paramount, at USD35 per Class A voting share and USD23.28 per Class B non-voting share—both representing a 33% premium over recent highs. The firm also plans to assume Paramount’s USD15.8 billion debt, pay a USD400 million break-up fee to Skydance Media, and inject USD10 billion in working capital into the media company, Reuters said. Neither Paramount nor National Amusements has confirmed the new offer. (Reuters) Update: The BusinessWire press release claiming that Apex Capital Trust had made a USD43 billion bid for Paramount Global was pulled by the PR service, Variety has reported. The release, issued at 10:32am ET, was widely quoted in news reports, including by Reuters and Bloomberg, leading to a spike in Paramount's share price. According to Variety, the announcement was pulled at 3pm ET, with no clarification from BusinessWire or Apex Capital Trust's PR representatives. Paramount declined to comment when contacted by Capital Brief, while Apex Capital Trust did not respond to an email seeking comment.

4.

Boeing leadership: Boeing appointed aviation veteran Kelly Ortberg as its new President and CEO, effective 8 August, taking him out of retirement to succeed David Calhoun, who is stepping down as the plane maker grapples with major operational and financial challenges. In a statement following the unveiling of a USD1.4 billion ($2.1 billion) quarterly loss, Boeing chairman Steven Mollenkopf said the 64 year old former Rockwell Collins CEO, will lead the century-old company “through this consequential period.” Boeing’s commercial jet business is embroiled in a quality crisis linked to deadly crashes and criminal fines. Despite retiring in 2021, Ortberg is respected by union leaders and analysts for fostering a strong culture at Rockwell, where he managed both its military and commercial divisions, and strengthened ties with airlines and the Pentagon while tackling similar challenges to those Boeing faces today, according to The Wall Street Journal. Boeing is also dealing with intense regulatory scrutiny, federal probes, congressional inquiries and supplier shortages. (Capital Brief)

5.

Japan hikes: The Bank of Japan (BOJ) raised interest rates for the first time in over a decade, hiking its benchmark rate 15 basis points to 0.25%. In a statement, the central bank cited concerns over the historically weak yen, leading to a jump in the Japanese currency, which strengthened to around 150-151 yen ($1.52-$1.53) per US dollar from over 154 yen the previous day. Governor Kazuo Ueda listed the yen’s decline, its impact on inflation and the economy as reasons for the hike. The BOJ also outlined plans to gradually reduce its government bond purchases by half to ¥3 trillion per month by early 2026. Some analysts, such as Moody’s economist Stefan Angrick, said the rate hike might hurt Japan's fragile economic recovery. (The Wall Street Journal)

6.

Political VC: Over 100 venture capitalists publicly pledged to vote for and support Democratic presidential candidate Kamala Harris in the 5 November election, including Shark Tank billionaire entrepreneur Mark Cuban, LinkedIn co-founder Reid Hoffman and billionaire investor Chris Sacca. In a statement on the website VCsForKamala.org, the group said the venture capital industry needs “strong, trustworthy institutions” without which the sector and any other would collapse. “That is what’s at stake in this election. Everything else, we can solve through constructive dialogue with political leaders and institutions willing to talk to us,” it said. “In this pivotal moment, we are united in our support for Vice President Kamala Harris.” The initiative comes as a response to the recent support for former President Donald Trump from some tech leaders, including Elon Musk and Marc Andreessen, amid a growing conservative influence in Silicon Valley. (The New York Times)

7.

Crude spike: Oil prices spiked following the assassination of Hamas leader Ismail Haniyeh in Tehran and recent Israeli strikes on Hezbollah, which heightened fears of regional conflict. Brent crude surged nearly 3% to USD80.81 ($123.74) per barrel, reflecting market concerns about the potential widening of the war in the Middle East after Iranian Supreme Leader Ali Khamenei vowed "severe punishment" against Israel for the attack. Israel has said that it doesn’t want to get into a war but that it is preparing for every scenario. Analysts warned of potential disruptions to the Strait of Hormuz, a crucial oil transit route through which roughly a fifth of global demand passes daily. A potential disruption there could not only hurt global trade and oil prices, but also impact inflation and the Fed’s monetary policies. Meanwhile, US crude oil inventories dropped more than forecast for the fifth consecutive week. (Fortune)

8.

Citi lapse: Citigroup repeatedly breached US Federal Reserve Regulation W, which limits intercompany transactions to protect depositors, Reuters reported citing an internal December 2023 document reviewed by the news agency. The breaches led to inaccuracies in the bank's liquidity reporting, according to the year-end regulatory snapshot document. The newly reported infractions are the latest in a series of regulatory issues for Citi, which has coped scrutiny and fines for its problematic risk management and internal controls since 2020. The bank was fined USD136 million for insufficient progress on compliance last month. Citi told Reuters it was “fully committed to complying with laws and regulations and have a strong Regulation W framework in place to ensure prompt identification, escalation and remediation of issues in a timely manner. The Federal Reserve declined to comment. (Reuters)