Waste of energy

An $80 billion Woodside-Santos merger made little sense from the beginning — including from an energy transition perspective, with the companies pursuing very different net zero strategies.

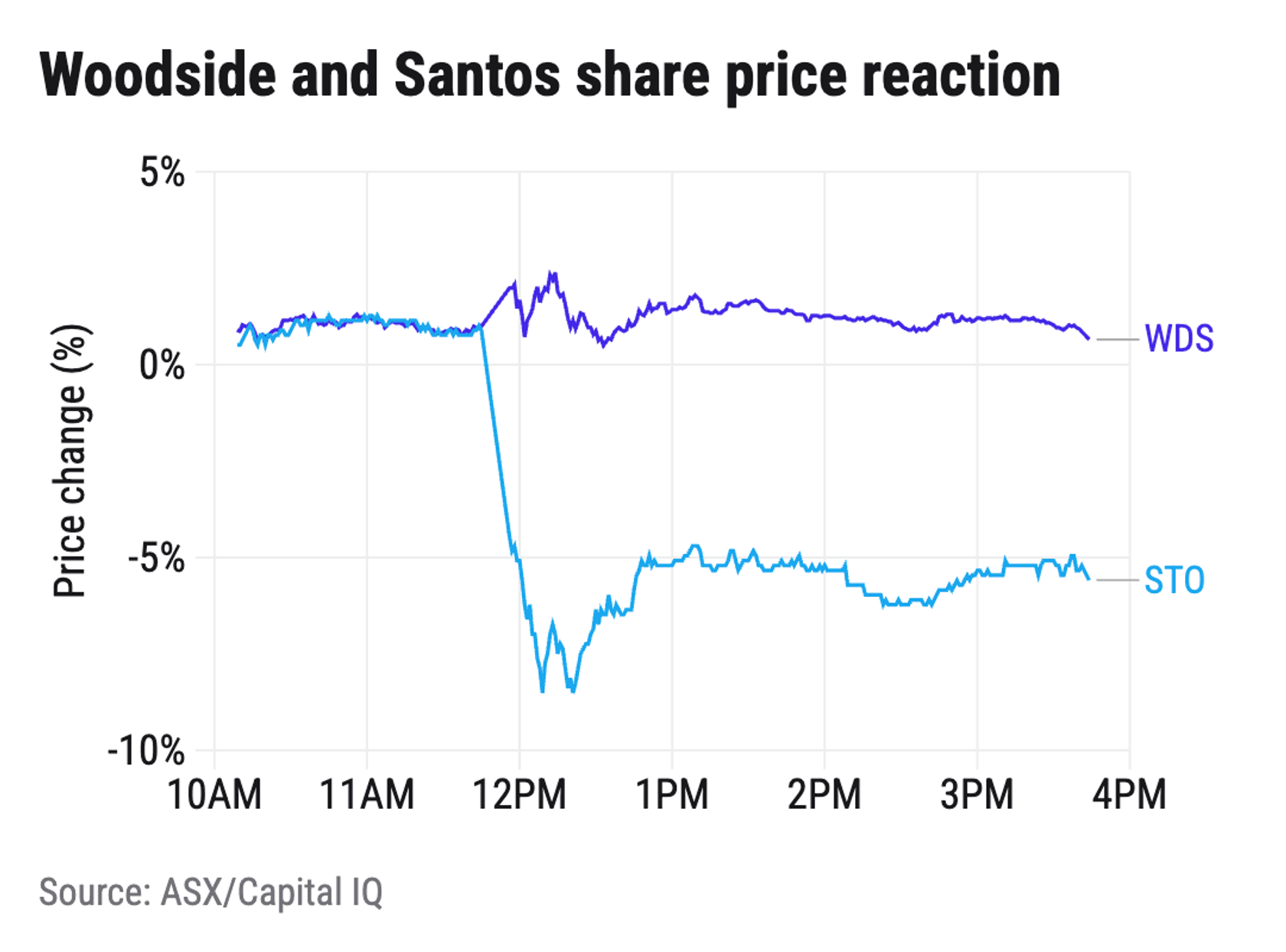

Woodside and Santos were tightlipped today when asked why their two month-long merger talks failed to result in a transaction.

But looking at the companies’ share prices post the announcement and after hedge funds betting on the deal unwound their trades, it's not hard to see which party stood to benefit the most from an $80 billion tie-up.

As seen in the chart below, Santos shares plunged minutes after Woodside issued its statement, before paring some of their losses, although it was still the ASX 200's worst performer today. Woodside shares headed in the other direction and ended higher for the day.

The fact that Woodside was first to broadcast the news has been interpreted as the company wanting to prove that it was least committed to a deal.